Editors Comments:

Those who have been following my blog's, posts and comments since last year are well aware that I have been very bearish on Australian real estate along with my own country Canada and most Western countries.

If the current state of the world economy continues I expect Australian real estate and most major wetern cities to drop 20% to 30% before it's all over.

Smart real estate investors should sell quickly even taking 10% decrease from previous prices and invest wisely in other places that are much greener such as Bali where prices have dropped during the pandemic 20% to 50% and are now moving rapidly back up.

Contact me direct at +62 8123-814-014 if you would like to discover great investment opportunities that are safe, starting as low as 75,000 USD

From https://www.news.com.au/finance/economy/interest-rates/why-sydney-and-melbourne-are-up-for-a-record-house-price-correction/news-story/fd6b4fb255cb6e1fb1504bde47fc33ff________________________________

If

the Reserve Bank continues lifting the cash rate, Sydney and Melbourne

are staring at their biggest house price corrections in living memory.

Leith van Onselen

July 17, 2022 - 1:24PM

While

most were expecting a rate increase, the 0.5 per cent hike caught many

off-guard. Here’s why the RBA locked in such a sharp jump.

More from interest rates

Swiss bank’s chilling prediction for Australia

Ray of hope despite record rental costs

RBA ‘failing’ due to surprising problem

Earlier

this month, the Reserve Bank of Australia (RBA) thrust a dagger into

the heart of mortgage holders when it lifted the cash rate by another

0.5 per cent – the third consecutive monthly increase.

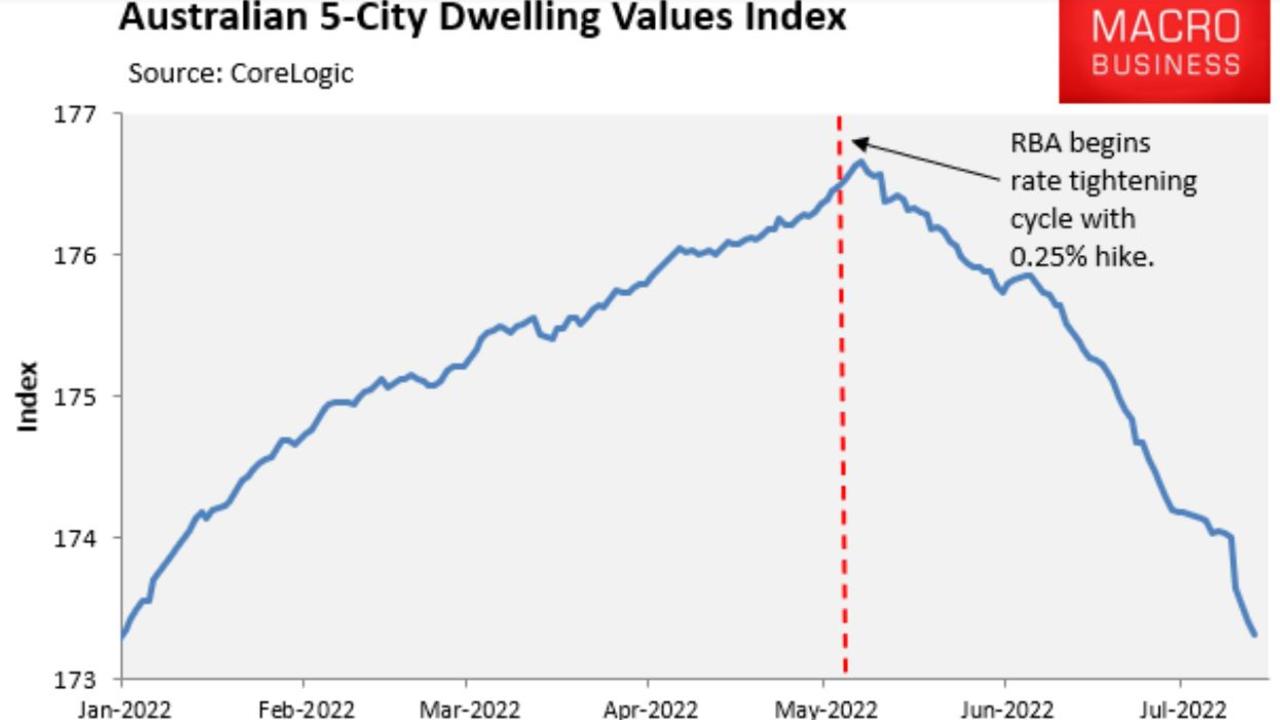

Dwelling values across Australia’s five major capital city markets began falling

shortly after the RBA’s initial 0.25 per cent rate hike in May, and

have so far fallen by around 2 per cent from their peak, according to

CoreLogic.

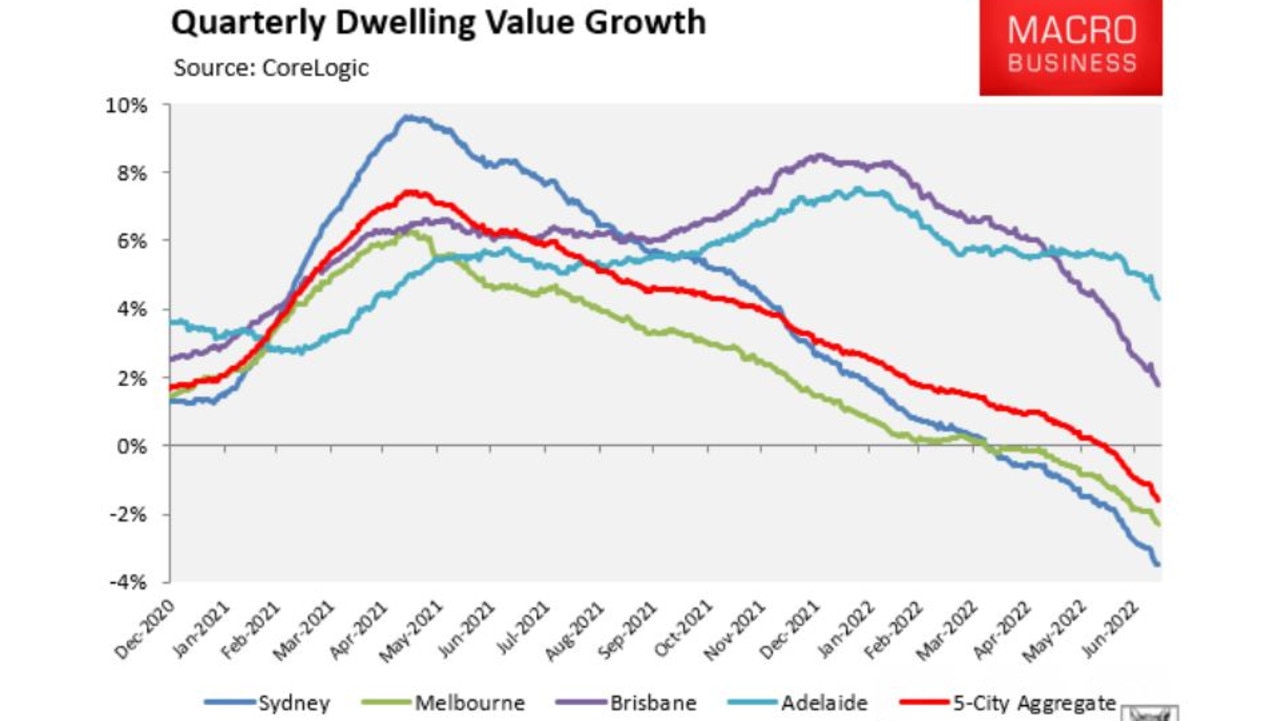

The

decline at the five-city aggregate level has been driven by Sydney and

Melbourne, where quarterly values have fallen by 3.5 per cent and 2.3

per cent respectively – more than offsetting growth across the smaller

markets:

AFR’s

latest survey of 31 economists revealed a median forecast for the

official cash rate (OCR) of 2.85 per cent by mid next year. If true,

Australia’s OCR would rise another 1.5 per cent from its current level.

The futures market remains even more hawkish, tipping a peak OCR of 3.5 per cent by May 2023.

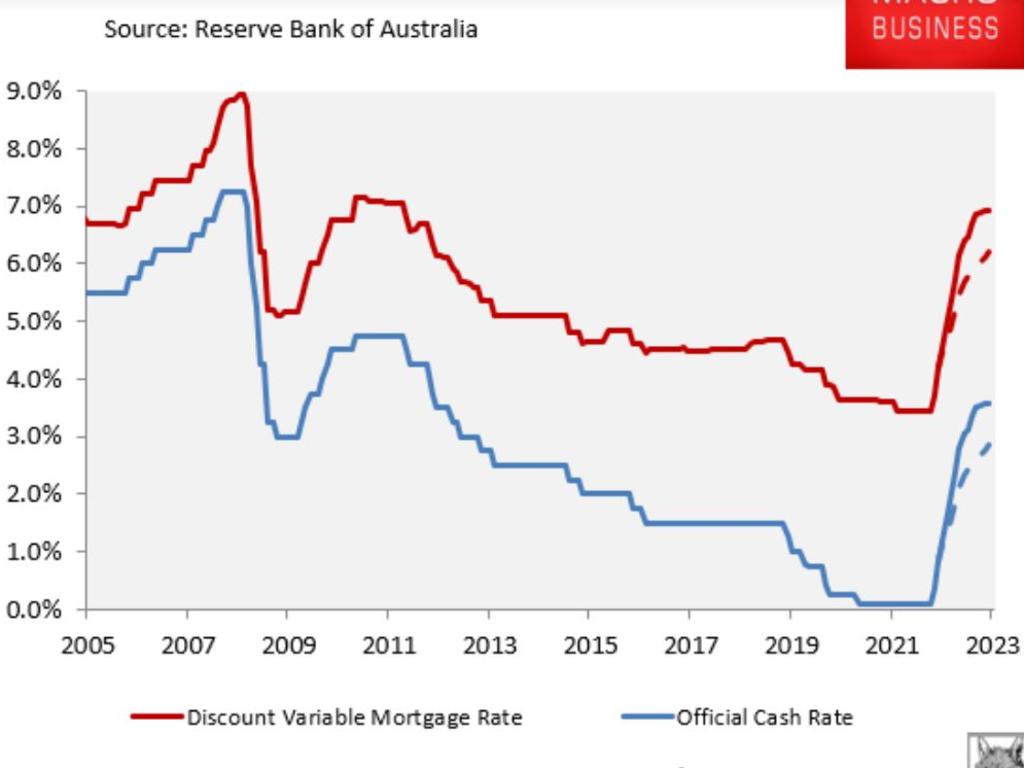

If

either interest rate forecast came true, it would see Australian

mortgage rates soar. Australia’s average discount variable mortgage rate

would climb to 6.2 per cent under the economists’ forecast (dashed red

line below) and to 6.8 per cent under the market’s forecast (solid red

line below):

The

market’s OCR forecast would mean that the discount variable mortgage

rate would climb to roughly double its level (3.45 per cent) before the

RBA’s tightening cycle began.

Under either scenario, Australian

mortgage holders would face a massive rise in repayments, which would

plunge many borrowers into severe financial stress at the same time as

the value of their properties falls sharply.

In its latest

Financial Stability Review, the RBA estimated “that a 200-basis-point

increase in interest rates from current levels would lower real housing

prices by around 15 per cent over a two-year period”.

Therefore,

the economists’ forecast 2.85 per cent OCR suggests a peak-to-trough

fall in real Australian house prices of around 20 per cent.

The

futures market’s forecast 3.5 per cent OCR would drive Australian

housing prices down by around 25 per cent in real terms under the RBA’s

modelling.

Sydney and Melbourne would likely face even bigger

price falls than the national average because they are the most

expensive housing markets with the most mortgage-indebted households.

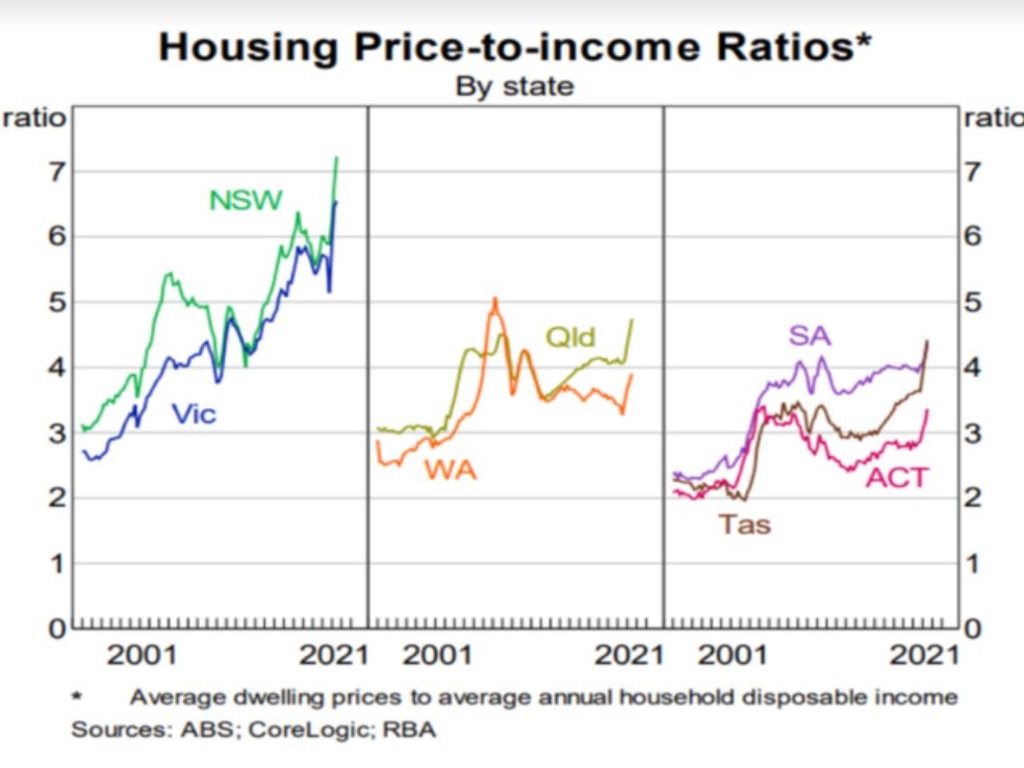

As illustrated in the next chart, the house price-to-income ratios for NSW (read: Sydney) and Victoria (read: Melbourne) are far higher than the other Australian jurisdictions:

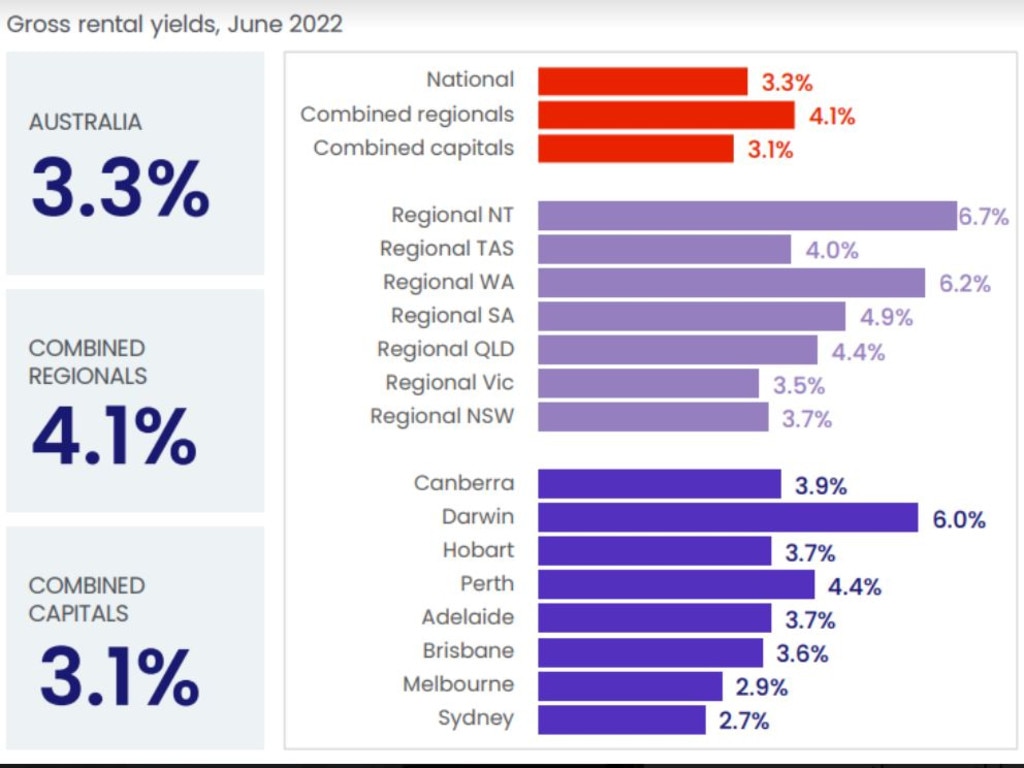

Sydney

and Melbourne are also the nation’s most expensive housing markets

relative to rents, as illustrated by their anaemic gross rental yields

of 2.7 per cent and 2.9 per cent respectively, according to CoreLogic:

Their

extreme valuations make Sydney and Melbourne more sensitive to the

RBA’s rate hikes, meaning their prices should fall further than the

national average under either the economists’ or the futures market’s

OCR forecast. The fact that these two markets are leading the current downturn is evidence enough.

Mortgage-holders

in our two largest cities better hope neither the economists nor the

market is correct, and that the RBA stops well short in its monetary

tightening.

More CoverageOne number that could stop rate risesScary truth behind RBA’s big gamble

Otherwise, Sydney and Melbourne are staring at their biggest price corrections in living memory.

Leith van Onselen is chief economist at the MB Fund and MB Super. Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

No comments:

Post a Comment