|

Center, Azizah & Her husband Lawrence Owners Pt. Bali Affordable Lifestyles International (PT. B.A.L.I.). Manage PT. Bali Luxury Villas, Best Asia Real Estate & Bali Luxury Retirement Villas. They & approximately 100 professional staff provide a one stop, efficient location for Buying, Selling, Leasing and Renting Asian Real Estate.

Editors Comments:

As our readers are well aware we have been bearish on the U.S. dollar for several months now.

It appears that many professionals are getting on board on that bearish call.

A falling U.S. dollar is good for Indonesia and Bali since many hotels & villas in Bali are priced on the Internet in U.S.D. Therefore if it takes less dollars to rent a villa or buy a home in Bali the demand will increase exponentially. A falling U.S. dollar is good for Indonesia and Bali since many hotels & villas in Bali are priced on the Internet in U.S.D. Therefore if it takes less dollars to rent a villa or buy a home in Bali the demand will increase exponentially.

The U.S. government has printed almost $4 trillion in the last couple years under the Trump administration with nothing to back it.

Many countries around the world such as China, Saudi Arabia, and even Japan are beginning to think that their investment in U.S.D. is not safe and looking for alternatives.

This could be the end of the U.S. dollar dominance for many years.

|

The argument that there is no alternative to the U.S. currency makes little sense. By

Stephen Roach

15 June 2020, 06:00 GMT+8

The dollar’s supremacy is threatened. Photographer: China Photos/Getty Images

The dollar’s supremacy is threatened. Photographer: China Photos/Getty ImagesStephen Roach, a faculty member at Yale University and former chairman of Morgan Stanley Asia, is the author of "Unbalanced: The Codependency of America and China."Read more opinion

Scorn has long been heaped on those daring to question the supremacy of the U.S. dollar as the world’s dominant reserve currency. I certainly received more than my fair share in reaction to a column I recently wrote for Bloomberg Opinion on the likelihood of a sharp decline in the greenback.

The counter-arguments were strong and highly political, basically boiling down to the so-called TINA defense – that when it comes to the dollar, “there is no alternative.”

That argument is very important in one critical sense: The dollar, like any foreign-exchange rate, is a relative price. As such, it encapsulates a broad constellation of a nation’s value proposition — economic, financial, social, and political — as viewed against comparable characterizations of other nations. It follows that shifts in foreign-exchange rates capture changes in these relative comparisons — the U.S. versus Europe, the U.S. versus Japan, the U.S. versus China, and so on.

My forecast that a 35% decline in the value of dollar could well be in the offing is couched in terms of the comparison between the U.S. and the currencies of a broad basket of America’s trading partners. Individual components in this basket are weighted by country-specific trade shares with the U.S. and expressed in real terms to capture shifting inflation differentials.

That argument is very important in one critical sense: The dollar, like any foreign-exchange rate, is a relative price. As such, it encapsulates a broad constellation of a nation’s value proposition — economic, financial, social, and political — as viewed against comparable characterizations of other nations. It follows that shifts in foreign-exchange rates capture changes in these relative comparisons — the U.S. versus Europe, the U.S. versus Japan, the U.S. versus China, and so on.

My forecast that a 35% decline in the value of dollar could well be in the offing is couched in terms of the comparison between the U.S. and the currencies of a broad basket of America’s trading partners. Individual components in this basket are weighted by country-specific trade shares with the U.S. and expressed in real terms to capture shifting inflation differentials.

As an economist, I care most about currency-related shifts in international competitiveness. The real effective exchange rate, or REER as calculated monthly by the Bank for International Settlements, is particularly well suited for this task.

In dissecting the TINA critique of the weak-dollar forecast, it helps to start with the weighting structure embedded in the REER to get a sense of which of the some 58 country-by-country relative comparisons might matter the most in pushing the BIS construct of the broad dollar index lower. Based on cross-border manufacturing trade flows, the BIS assigns the largest weights to China (23%), the euro area (17%), Mexico (13%), Canada (12%), and Japan (7%). These five countries (region in the case of the euro area) account for 72% of the total trade weights in the broad U.S. dollar index. An additional 13% comes from countries six through 10: South Korea, the U.K., Taiwan, India and Switzerland. Weights of the top 10 account for 85% of America’s cross-border trade.

On this basis, a forecast of a weaker dollar requires some combination of a strengthening in China’s renminbi and the euro. The currencies of America’s USMCA partners (formerly NAFTA) — Mexico and Canada — also matter a good deal in that they account for 25% of U.S. manufacturing trade. The yen is now of little consequence to movements in the broad dollar index, given its sharply reduced trade weight.

The China call is very contentious. From the trade war to the coronavirus war to the distinct possibility of a new Cold War, the negative case for China has never been stronger in the U.S. than it is today. Notwithstanding these concerns, the broad renminbi index constructed by the BIS is up 53% from its December 2004 lows in real effective terms. As long as China stays the course of structural reform — shifting from manufacturing to services, from investment- and export-led growth to consumer-led growth — and embraces a further liberalization of its financial system, the case for further currency appreciation remains compelling, even in the face an increasingly fraught relationship with the U.S.

The call on the euro is also counterintuitive, especially for a broad consensus of congenital euro-skeptics like me. That goes back to my Morgan Stanley days when I argued that an incomplete currency union — especially the lack of a pan-European fiscal transfer mechanism — could not withstand the inevitable stress of asymmetrical shocks.

I now have to concede that reports of the euro’s imminent death have been greatly exaggerated. Time and again, especially over the past 10 years, Europe has risen to the occasion and avoided a catastrophic collapse of its seemingly dysfunctional currency union. From Mario Draghi’s 2012 promise to do “whatever it takes” to save the euro from a sovereign debt crisis to the recent Angela Merkel-Emmanuel Macron commitment to a Next Generation European Union Fund of 750 billion euros ($855 billion) to address the coronavirus crisis, the great European experiment has endured extraordinary adversity. With the trade-weighted euro 15% below its April 2008 high, there is unmistakable upside for the most unloved currency in the world.

With China and the euro zone accounting for 40% of U.S. trade, I would be the first to concede that the math of a dollar crash won't add up unless those two currencies rise significantly, as I expect. Moreover, with both economies plagued by long standing current-account surpluses — albeit sharply reduced in China in recent years — currency appreciation is the classic cure for such imbalances.

Movements in other currencies should reinforce that outcome. That is especially true of yen, which should draw support from Japan’s relatively successful Covid-19 containment strategy. The same can be expected from the U.S.’s USMCA partners, Mexico and Canada, both of whose currencies were hit hard earlier this year by the lethal combination of the coronavirus shock and a stunning collapse in world oil prices.

The plunge in the peso was exaggerated by an unwinding of so-called carry trades during the meltdown of U.S. equities in late March. Barring a double-dip recession in the global economy, haven plays into the dollar should unwind over the balance of 2020 and into 2021, reinforcing the negative case for the dollar. And although cryptocurrencies and gold should benefit from dollar weakness, these markets are too small to absorb major adjustments in world foreign-exchange markets where daily turnover runs around $6.6 trillion.

Alas, the TINA argument doesn't stop there. The counter to my case for dollar weakness also rests on the reserve status of the U.S. currency as the linchpin of world financial markets. All trading nations, goes the argument, have to hold the dollar as the price for doing business in an increasingly integrated dollar-based world economy.

Even so, the dollar’s share of official foreign-exchange reserves has declined from a little over 70% in 2000 to a little less than 60% today, according to the BIS. That downtrend could gather momentum in the years ahead, especially with the U.S. currently leading the charge in de-globalization and decoupling. With America’s share of reserves well in excess of its share in world GDP and trade, such a correction might well be inevitable in an increasingly fragmented, multi-polar world.

If TINA is the dollar’s only hope, look out below. America’s saving and current-account problems are about to come into play with a vengeance. And the rest of the world is starting to look less bad. Yes, a weaker dollar would boost U.S. competitiveness, but only for a while. Notwithstanding the hubris of American exceptionalism, no leading nation has ever devalued its way to sustained prosperity.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

To contact the author of this story:

Stephen Roach at stephen.roach@yale.edu

To contact the editor responsible for this story:

Robert Burgess at bburgess@bloomberg.net

In dissecting the TINA critique of the weak-dollar forecast, it helps to start with the weighting structure embedded in the REER to get a sense of which of the some 58 country-by-country relative comparisons might matter the most in pushing the BIS construct of the broad dollar index lower. Based on cross-border manufacturing trade flows, the BIS assigns the largest weights to China (23%), the euro area (17%), Mexico (13%), Canada (12%), and Japan (7%). These five countries (region in the case of the euro area) account for 72% of the total trade weights in the broad U.S. dollar index. An additional 13% comes from countries six through 10: South Korea, the U.K., Taiwan, India and Switzerland. Weights of the top 10 account for 85% of America’s cross-border trade.

On this basis, a forecast of a weaker dollar requires some combination of a strengthening in China’s renminbi and the euro. The currencies of America’s USMCA partners (formerly NAFTA) — Mexico and Canada — also matter a good deal in that they account for 25% of U.S. manufacturing trade. The yen is now of little consequence to movements in the broad dollar index, given its sharply reduced trade weight.

The China call is very contentious. From the trade war to the coronavirus war to the distinct possibility of a new Cold War, the negative case for China has never been stronger in the U.S. than it is today. Notwithstanding these concerns, the broad renminbi index constructed by the BIS is up 53% from its December 2004 lows in real effective terms. As long as China stays the course of structural reform — shifting from manufacturing to services, from investment- and export-led growth to consumer-led growth — and embraces a further liberalization of its financial system, the case for further currency appreciation remains compelling, even in the face an increasingly fraught relationship with the U.S.

The call on the euro is also counterintuitive, especially for a broad consensus of congenital euro-skeptics like me. That goes back to my Morgan Stanley days when I argued that an incomplete currency union — especially the lack of a pan-European fiscal transfer mechanism — could not withstand the inevitable stress of asymmetrical shocks.

I now have to concede that reports of the euro’s imminent death have been greatly exaggerated. Time and again, especially over the past 10 years, Europe has risen to the occasion and avoided a catastrophic collapse of its seemingly dysfunctional currency union. From Mario Draghi’s 2012 promise to do “whatever it takes” to save the euro from a sovereign debt crisis to the recent Angela Merkel-Emmanuel Macron commitment to a Next Generation European Union Fund of 750 billion euros ($855 billion) to address the coronavirus crisis, the great European experiment has endured extraordinary adversity. With the trade-weighted euro 15% below its April 2008 high, there is unmistakable upside for the most unloved currency in the world.

With China and the euro zone accounting for 40% of U.S. trade, I would be the first to concede that the math of a dollar crash won't add up unless those two currencies rise significantly, as I expect. Moreover, with both economies plagued by long standing current-account surpluses — albeit sharply reduced in China in recent years — currency appreciation is the classic cure for such imbalances.

Movements in other currencies should reinforce that outcome. That is especially true of yen, which should draw support from Japan’s relatively successful Covid-19 containment strategy. The same can be expected from the U.S.’s USMCA partners, Mexico and Canada, both of whose currencies were hit hard earlier this year by the lethal combination of the coronavirus shock and a stunning collapse in world oil prices.

The plunge in the peso was exaggerated by an unwinding of so-called carry trades during the meltdown of U.S. equities in late March. Barring a double-dip recession in the global economy, haven plays into the dollar should unwind over the balance of 2020 and into 2021, reinforcing the negative case for the dollar. And although cryptocurrencies and gold should benefit from dollar weakness, these markets are too small to absorb major adjustments in world foreign-exchange markets where daily turnover runs around $6.6 trillion.

Alas, the TINA argument doesn't stop there. The counter to my case for dollar weakness also rests on the reserve status of the U.S. currency as the linchpin of world financial markets. All trading nations, goes the argument, have to hold the dollar as the price for doing business in an increasingly integrated dollar-based world economy.

Even so, the dollar’s share of official foreign-exchange reserves has declined from a little over 70% in 2000 to a little less than 60% today, according to the BIS. That downtrend could gather momentum in the years ahead, especially with the U.S. currently leading the charge in de-globalization and decoupling. With America’s share of reserves well in excess of its share in world GDP and trade, such a correction might well be inevitable in an increasingly fragmented, multi-polar world.

If TINA is the dollar’s only hope, look out below. America’s saving and current-account problems are about to come into play with a vengeance. And the rest of the world is starting to look less bad. Yes, a weaker dollar would boost U.S. competitiveness, but only for a while. Notwithstanding the hubris of American exceptionalism, no leading nation has ever devalued its way to sustained prosperity.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

To contact the author of this story:

Stephen Roach at stephen.roach@yale.edu

To contact the editor responsible for this story:

Robert Burgess at bburgess@bloomberg.net

Coronavirus Special

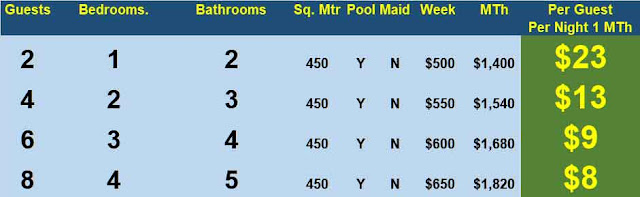

Huge Luxury Villas & Estates Start at $6.00 per GuestOffered by one of Bali's oldest, largest and most reputable villa and estate managers PT. Bali Luxury Villas. is offering these unbelievable low prices until July 15th. 2020

Normal prices are $20-$40 this is a 70% to 85 % discount.

Bali Luxury Villas or a Bali Paradise Beachfront Estate at unbelievable prices.

*Prices include a private housekeeper 5.5 days per week. It does not include 11% tax or electricity.

These prices are specifically designed for those who wish to improve their lifestyle while under self-quarantine in Bali in addition to those who wish to escape from places such as Jakarta, Surabaya, and other major cities where coronavirus may get horrific before it's over.

Huge Villas & Estates:

These large 350 m to 650 m² meter private villas and estates offer maximum protection against coronavirus in that there is no one close enough to cause you or your family to get the virus.

Most offer a private full-time housekeeper who will come each day with plastic gloves, plus mask and take care of all your household needs such as cleaning the floors, washing the windows, cleaning the dishes and making the beds.

Most offer a private full-time housekeeper who will come each day with plastic gloves, plus mask and take care of all your household needs such as cleaning the floors, washing the windows, cleaning the dishes and making the beds.

Free Laundry:

One of the nicest perks is the free laundry with private laundry facilities.

As these villas are located in the Village of Sanur they are within walking distance to the beach and dozens if not hundreds of restaurants which although may be closed they are open for delivery and take away.

You'd never need to leave your Villa because there are services available for everything including delivering groceries from fruits and vegetables to meats and even Australian pies.

Large Kitchen, Dining & Living Area:

Each kitchen has its own large marble and teak kitchen with a full-size refrigerator and four-burner stove plus all the appliances to make your stay comfortable. Remember you won't have to do the dishes most of the time because a housekeeper will take care of that.

Best of all they all have a private swimming pool from 9 m to 14 m in the beachfront estates.

During this time, it is essential to keep your self healthy and fit. No better way to do that then 10 -20 laps in your own 9-14 meter. swimming pool.

Fiber Optic Wi-Fi, TV and Telephone:

You also have high-quality Wi-Fi, fiber-optic television and telephone to keep in contact with your friends and relatives.

Award-Winning 24 Hr. Management:

The villas and estates are managed by PT. Bali Affordable Lifestyles International who will provide you free gardening, pool cleaning service and a private housekeeper, reception service,, and maintenance services.

TOP 2% of Hotels In The World:

This year they received the coveted Tripadvisor Hall of Fame Award after receiving their Certificate of Excellence Award each year for the past ten years.

This places them among the top 2 % of hotels and villas listed by Tripadvisor worldwide.

Limited Villas Book Now to Avoid Disappointment:

Interested parties please contact me. Lawrence, directly at 62-8123814014 Email: lbptbali@gmail.com

Or our Rentals Manager: Yanthi at +62 815-5890-0389 or our Reception at PT Bali Luxury Villas at 62-361-284069

To share this information copy this link & send https://baliworldnewsviews.blogspot.com/2020/06/bali-to-target-tourists-from-nearby.html

Bali Paradise Beach Estates

Coronavirus Special.

Starting at a $8.00 Per Person a

70 -80 % Discount

Enjoy this 450 m2 Four-bedroom, Five bathroom Estate in a quite beachfront complex all to yourself.

Live your dream and wake up to the sound of crashing waves and an amazing view of the sun rising over the Channel Islands.

The stunning 3,200 MTR. Mt. Agung, Volcanic Mountain will reach out and touch you most mornings.

It Is located on a Beach named by the locals as Pantai Purnama which mean Full Mean Beach.

If you book during a full moon you will understand why.

This estate is ideally located only 15 minutes from Sanur and 25 minutes from Ubud, two of Bali's top five resort areas.

The view from this estate

Enjoy your own private walkway to the beach. Magical walks on the remote beach which runs for 30 km and the sound of exotic birds will make you never want to leave.

The Estate:

Built by Award Winning Bali Developer:

This luxurious estate was built a few years ago by one of Bali's leading luxury Villa developers.

He spared no cost and installed solid marble flooring, kitchen tops, and bathroom fixtures.

A key feature of the estate is a 14 meter, 45 ft. private swimming pool which has several areas for children. This will keep you in shape and healthy during this difficult time plus provide hours of pleasure for you and your family. A Gardener and Pool Man is included.

First-class furniture, beds, and bathroom fixtures can be enjoyed throughout.

A two-person Jacuzzi tub compliments the huge master bedroom.

Guest access:

Guests can freely walk about the almost 1 Hectare complex which includes private access to the beach.

Other things to note:

Whether you rent one bedroom or four bedrooms you will have private use of the entire four-bedroom estate including a private 14 m swimming pool.

100% Privacy:

The ground floor with the pool and the gardens are completely enclosed by a high wall which gives you 100% privacy and security.

There is only one other estate in this complex at this time.

Beautiful Saba River Only five minutes walk.

Best of all the only other Estate in the complex is owned by the owners of this rental estate Aziah and Lawrence.

Lawrence is an experienced 17-year Bali hotel manager and his wife is an Indonesian Notaris.

Lawrence is a Superhost on Airbnb. Superhosts are experienced, highly rated hosts who are committed to providing great stays for guests. They also have the Hall of Fame award from Tripadvisor.

The Owners Lawrence and Notaris/Spouse Azizah at their home at Bali Paradise Beach Estates

Interested parties please contact me. Lawrence, directly at 62-8123814014 Email: lbptbali@gmail.com or our Rentals Manager Yanthi at +62 815-5890-0389 or our Reception at PT Bali Luxury Villas at 62-361-284069

Prices are up to 70 % off Normal for the next few Months. Start at $8.00.

*Prices does not include 11% tax or electricity.

*Prices does not include 11% tax or electricity.Limited Villas Book Now to Avoid Disappointment:

Interested parties please contact me. Lawrence, directly at 62-8123814014 Email: lbptbali@gmail.com

Or our Rentals Manager: Yanthi at +62 815-5890-0389 or our Reception at PT Bali Luxury Villas at 62-361-284069

To share this information copy this link & send https://baliworldnewsviews.blogspot.com/2020/06/bali-to-target-tourists-from-nearby.html

Bali Luxury Retirement Villas

Only 2.98 Milyar (* $184,888 U.S.D. or$268,888 Aus.)

You may now Invest, Vacation or retire full time or part-time in Bali while achieving very handsome returns with this freehold property for Indonesian buyers or over 80 years of leases for Foreign Buyers included in the purchase price starting at USD 184,888.

Pretty well everything you need to know including location, prices, and designs plus information on Bali and Bali retirement visas is available on our web site https://www.baliluxuryretirementvillas.com.

These brand-new luxury retirement villas are located only 200 m or a three minute walk from one of the best beaches on the east coast of Bali.

Swimming, snorkeling, surfing, horseback riding, and several new high-quality beach clubs are within walking distance.

The following Information is available on our website:

Features of © Bali Luxury Retirement Villas as low as * $184,888.

•100% legal for foreigners.

• Includes leases totaling 80 yrs.

• Private carport included.

• Private 8 m (27 Ft.) pool** for leisurely laps.

• Only 200 Mtr. To a fabulous beach, restaurants, beach clubs.

• Great investment for you and your heirs.

• Private Housekeepers & drivers, only $200 MTh.

• Healthcare at a fraction of Western costs.

• Brand-new hospital within five minutes.

• Award-winning International Airport 35 min.

• Proximity to Sanur, Ubud, Denpasar.

• Walking distance to affordable restaurants and beach clubs

• Shared low costs of pool man and gardeners.

• Minuscule monthly common area fees.

• Managed by 15-year-old, Hall of Fame award-winning management company.

• *Price of the least expensive villa in U.S.D. after $10,000 Discount for the first two villas only. Subject to change without notice.

Developed and managed by 14-year-old Hall of Fame award-winning Bali company.

Our 15-year-old Bali company Pt. Bali Affordable Lifestyles International (PT. B.A.L.I.) with over 100 + staff and thousands of satisfied clients guarantee completion of any villas purchased now in 2020.

We are a Ten-Year Consecutive “Certificate of Excellence” recipient on the World's Largest Travel Site and was awarded their "Hall of Fame Award", in 2019. This is awarded to only 2 % of the Hotels & Villas listed on TripAdvisor Worldwide"

Summary:

Profit Now Move in Later:

These villas offer you an opportunity to own a luxury home on arguably the Best Island in the world with some of the greatest weather, lowest cost of living, clean air, and friendliest people.

Profit Now Move in Later:

You may not be ready to pack up and move to Bali in the next few years.

So, you may purchase now at these ridiculously low prices and we can normally rent them out for you for a monthly income of $1,500 to $2,000 U.S.D. per month.

Our 15-year-old “Hall of Fame” the award-winning management company that manages villas for V.I.P.s such as the former director of General Electric and Ritz Carlton can provide substantial net monthly income to supplement your pension while providing a carefree rental unit.

Confused? We understand that you may have concerns that we may not have even thought of, so feel free to ask whatever questions you wish.

We do not want you to even think about purchasing our © Bali Luxury Retirement Villas unless you are 100% convinced that they are safe, and perfect for you and your family.

Limited Offer: Save $10,000: As with any new project we are anxious to sell the first few villas.

We have one already on hold and are only willing to offer one other villa at a $10,000 discount. First come first serve.

Free Stay in Luxury Estate:

If you wish to fly over and see the location first after you place a USD $2,000 Deposit we will offer you free accommodations in a 4 bdrm, 5 bath luxury beach view estate with a private 14 m pool for three days within walking distance of the location.

When you decide to conclude the purchase, we will extend the free estate accommodation for an additional four days.

Should you decide not to continue with the purchase we will refund your $2,000 Deposit minus $200.00 for the three-day stay.

Cheers, THE SALES TEAM © Bali Luxury Retirement Villas

PLEASE CALL OR EMAIL US: Tel: 62-361-284069 Mobile or Whatsapp 62-812-3814014 Email: infoBLRV@gmail.com

P.S. We also have several larger villas available from two-bedroom to four-bedroom starting as low as $158,888. www.baliluxuryvillasales.com

To share this information copy this link & send https://baliworldnewsviews.blogspot.com/2020/06/bali-to-target-tourists-from-nearby.html

Save $100,000 On Huge Estate

Only $488,888 Freehold or 80 year leases

For those of you that want to live in luxury for a fraction of Western costs we have this magnificent four bedroom five bathroom 450 m² luxury estate with a private beach entrance in a beachfront complex with views to die for.

Please contact us if you wish for further information. Tel: 62-361-284069 Mobile or Whatsapp 62-812-3814014 Email: infoBLRV@gmail.com

Are you tired of traditional investments such as banks and bonds that only offer 1%- 6% per year, which may not keep pace with the real inflation?

Do you want to become rich the way over 60 % of self-made multi-millionaires did?

“Become rich the way over 60 % of self-made multi-millionaires did?”

According to PT. B.A.L.I., one of Bali's leading real estate experts for the past 14 years, who have thousands of satisfied clients, this is the “Second best time to purchase Bali Real Estate this century”.

“Second best time to purchase Bali Real Estate this century”.

Recent recent clarification of Bali real estate laws for foreigners allowing them to obtain control of Bali Real Estate for more than normal life is creating a huge new demand for Indonesian and Bali Real Estate.

Coupled with the fact that Bali Real Estate has recently undergone the first correction in modern history with prices down as much as 50 % this may have set the stage for *increases of 20 % to 100 % in the next three to five years.

Free Bali Real Estate Seminar Video:

Whether you are a buyer, seller, broker, agent, investor, lessor or renter you can benefit from viewing PT. B.A.L.I’s latest Free Bali Real Estate Seminar Video filmed just a few months ago.

At this seminar PT. B.A.L. I’s Canadian President, a 23 yr. Bali resident, who is married to a fully Licenced Indonesian Notaris reviewed the most recent real estate laws for Indonesians and Foreigners in detail.

He also discussed the Past, Present, and Future of Bali Real Estate.

Click Here to view the latest Free Bali Real Estate Seminar Video

Free Seminar Topics:

Free Seminar Topics:

During this Free Bali Seminar Video you will learn about:

>The Past, Present and Future of Bali and Indonesian real estate.

>Why a recent official clarification of foreign ownership laws allows foreigners to totally control Indonesian properties for up to 80 years.

> How to avoid legal problems and make sure a property is safe.

> How to avoid complicated real estate laws - Indonesians married to foreigners.

> Why this is the second-best time to buy this century.

> Where are the best locations to buy for maximum profits?

> What type of properties will offer the best potential of *10% to 20 % per year?

> Discover how you can sell your property fast for the highest prices and lowest commissions.

> An opportunity for a free listing on B.A.R.E.

> First Class Beachfront property at almost 50% discount.

> A Quality 5,000 m2 Bali Hotel with 12 bungalows, 3 pools, and Restaurant for only $588,000.

> Low-cost properties with Luxury Villas starting as low as $158,888 for a three-bedroom 650 m² 3-bedroom, 4 - bath with private 9 - meter. Pool in Sanur.

> Ridiculously low-priced ocean view building lots starting as low as $25,000 for 500 m².

> Brand New Bali Luxury Retirement Villas starting at

To share this information copy this link & send https://baliworldnewsviews.blogspot.com/2020/06/bali-to-target-tourists-from-nearby.html

Note from The Seminar Speaker:

After living in Bali for 23 years and running a Development and Real Estate Company for the last 18 years plus the fact that I'm married to a full lead licensed Notaris I think you will find that everything that you need to know about Bali Real Estate is covered in this timely seminar.

>Why a recent official clarification of foreign ownership laws allows foreigners to totally control Indonesian properties for up to 80 years.

> How to avoid legal problems and make sure a property is safe.

> How to avoid complicated real estate laws - Indonesians married to foreigners.

> Why this is the second-best time to buy this century.

> Where are the best locations to buy for maximum profits?

> What type of properties will offer the best potential of *10% to 20 % per year?

> Discover how you can sell your property fast for the highest prices and lowest commissions.

> An opportunity for a free listing on B.A.R.E.

> First Class Beachfront property at almost 50% discount.

> A Quality 5,000 m2 Bali Hotel with 12 bungalows, 3 pools, and Restaurant for only $588,000.

> Low-cost properties with Luxury Villas starting as low as $158,888 for a three-bedroom 650 m² 3-bedroom, 4 - bath with private 9 - meter. Pool in Sanur.

> Ridiculously low-priced ocean view building lots starting as low as $25,000 for 500 m².

> Brand New Bali Luxury Retirement Villas starting at

To share this information copy this link & send https://baliworldnewsviews.blogspot.com/2020/06/bali-to-target-tourists-from-nearby.html

No comments:

Post a Comment